In the ever-evolving landscape of the plastics industry, understanding what your commercial

insurance policies do and do not cover is more critical than ever. The recent attention on PFAS

(per- and polyfluoroalkyl substances) and their associated legal challenges underscores the

necessity for plastics processors to be on high alert. PFAS, often termed “forever chemicals”

due to their persistence in the environment, have become a focal point for lawsuits and

regulatory scrutiny.

Insurance Policy Exclusions

Product liability coverage is essential, and it is important to be aware of potential exclusions in

policies, particularly concerning PFAS exposure. Many insurers are adding specific exclusions

for PFAS-related claims due to these substances’ excessive costs and liabilities. In addition to exclusions added to general liability policies, these exclusions also appear on umbrella/excess policies, which reduce coverage if the underlying policies do not contain PFAS exclusions.

Even if your insurance carrier does not currently have these exclusions, we anticipate most will

soon follow suit and add them. We suggest watching your renewal for these endorsements, as

many carriers are including these on renewals in 2024.

Depending on your insurance carrier, the title or policy form number pertaining to PFAS

exclusions can vary. The ISO (Insurance Services Offices) form that a lot of insurance carriers

use is:

- CG 34 95 Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances to use with products/completed operations liability coverage part or Owners and Contractors protective liability coverage part

- CG 34 96 Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances, to use with the railroad protective liability coverage part

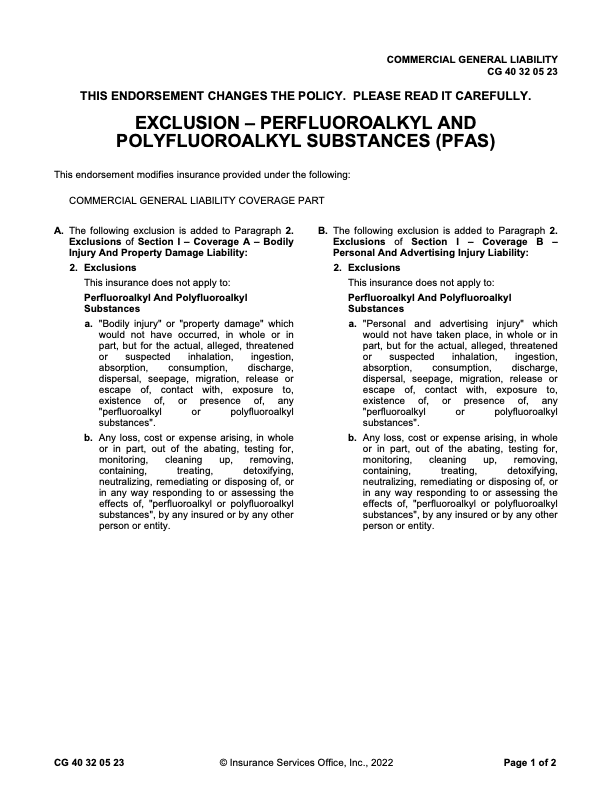

- CG 40 32 Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances to use with the commercial liability coverage part

- CU 34 54 Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances (PFAS), to use with the commercial liability umbrella coverage part

- CX 21 97 Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances (PFAS), to use with the commercial excess liability coverage part

- For the Business Owners Policy – BP 15 91, Exclusion – Perfluoroalkyl And Polyfluoroalkyl Substances (PFAS)

The general liability endorsement, as seen below, modifies the Commercial General Liability

Coverage Part by adding a total exclusion for PFCs and PFAS. It specifies that the insurance

does not cover any:

- Bodily injury

- Property damage

- Personal and advertising injury related to PFC/PFAS exposure

- Design, manufacturing, sale, or disposal of PFC/PFAS

- Costs associated with testing, monitoring, cleaning up, or responding to PFC/PFAS

- Exclusion applies even if claims allege negligence or wrongdoing in supervision or other

areas by the insured.

Regardless of how PFAS exclusions are addressed in your commercial policy, such exclusions

can leave plastics processors vulnerable to significant financial risk if not properly addressed.

Therefore, understanding the specifics of your insurance policy and negotiating coverage (if

available) that minimizes these exclusions is crucial for comprehensive protection.

Moving Forward: Best Practices for Plastics Producers

To effectively manage risks and ensure adequate coverage, plastics processors should

consider the following best practices:

- Regular Insurance Reviews: Periodically review and update insurance policies to align with the latest industry risks and regulatory requirements.

- Training and Awareness: Investing in ongoing employee training about the risks associated with PFAS and other hazardous chemicals. Building a culture of safety and compliance can significantly reduce the likelihood of incidents.

- Collaboration with Legal and Environmental Experts: To stay ahead of emerging risks and regulatory changes, work closely with legal counsel and environmental experts. This collaboration can provide valuable insights and help develop comprehensive risk management strategies.

The Bottom Line

The heightened focus on PFAS and their associated risks serves as a powerful reminder of the

importance of risk mitigation and appropriate insurance coverage for plastics manufacturers. By

implementing proactive risk management strategies and securing comprehensive insurance,

companies can navigate the complex landscape of environmental and legal challenges,

ensuring long-term stability and success in the industry.

A firm with deep expertise in commercial insurance and risk mitigation for plastics processors, BakerHopp is here to help you assess your risks and find the right coverage to protect your business. Contact us today to learn more about how we can support your risk management efforts.