Updated as of 07/16/24

Overall Outlook

The last two years of volatility in the commercial insurance marketplace have contributed to what an insurance company executive recently referred to as “a very unique time in the industry.” The first quarter of 2024 marked the 25th consecutive quarter of firming pricing for the US Commercial Lines market, and the outlook is that the rates will remain firm throughout 2024 and likely 2025. One industry expert, David Paul of Leader’s Edge, refers to this protracted time as an “Atypical Hard Market,” and he describes the factors contributing to these market conditions below:

What is Behind this Atypical Hard Market?

- Persistent economic and social inflation has produced much higher losses and loss adjustment costs than anticipated by pricing actuaries

- Greater insured losses from weather-related events across a broader swath of the United States, again unanticipated and still seemingly impossible to model

- Much more expensive and scarce reinsurance protection, especially for property coverage

- A 15-year run of historically low interest rates (note: investment income historically accounts for the lion’s share—if not, at times, all—of P&C operating profitability)

Outlook By Line of Coverage: Property

For the first quarter of 2024, 10.1% was the average commercial property premium increase.

While the average increase was lower than last quarter, 10.1% is still the highest of all lines. Commercial property is one of the most difficult lines of coverage at renewal due to stricter underwriting, property value increases and the amount of detail required in submissions to insurance carriers.

Commercial property insurance continues the uphill battle against uncontrollable weather conditions. The frequency and severity of natural disasters such as hurricanes, wildfires, and floods have risen sharply. Insurers face higher claims payouts, leading to increased premiums to offset these costs.

Image by the National Oceanic and Atmospheric Administration at the National Centers for Environmental Information via https://www.ncei.noaa.gov/access/billions/time-series

Also having a significant impact on property insurance rates and underwriting is reinsurance (also known as the insurance for insurers). Reinsurance plays a pivotal role in the insurance industry, acting as a safety net for insurance companies by helping them manage risk and maintain financial stability. The continuation of paying out claims for natural disasters, inflation impacting the cost per claim, and poor investment returns are driving up reinsurance premiums and increased retentions for insurance companies, which is partially passed through to policyholders.

Outlook by Line of Coverage: Casualty

For the first quarter of 2024, 4.1% was the average commercial casualty premium increase.

Social inflation continues to drive up premiums, create a selective underwriting environment, and force restrictive coverage terms and conditions. The term social inflation was introduced to the industry in the past few years and describes the rising costs of insurance claims resulting from increased legal advertising, expansion of the litigation finance sector, broader definitions of liability, more plaintiff-friendly legal decisions, and larger compensatory jury awards. Currently, these activities are having a more significant impact on the commercial auto market. However, the industry is starting to see the impact in general liability cases. The industry continues to push for tort reform across the country.

CASUALTY RENEWAL PRICING BY LINE OF COVERAGE

| Type of Coverage | 2024 Second Half Forecast |

| General Liability | +5% to 10% |

| Auto Liability | +5% |

| Workers Compensation | -10% |

| Umbrella | +1% to 12.5% |

| Foreign Liability | Flat |

| Directors and Officers | -5% |

| Employment Practices Liability | -5% to +5% |

| Professional Liability | +1% to 10% |

| Cyber Liability | -10% to +1% |

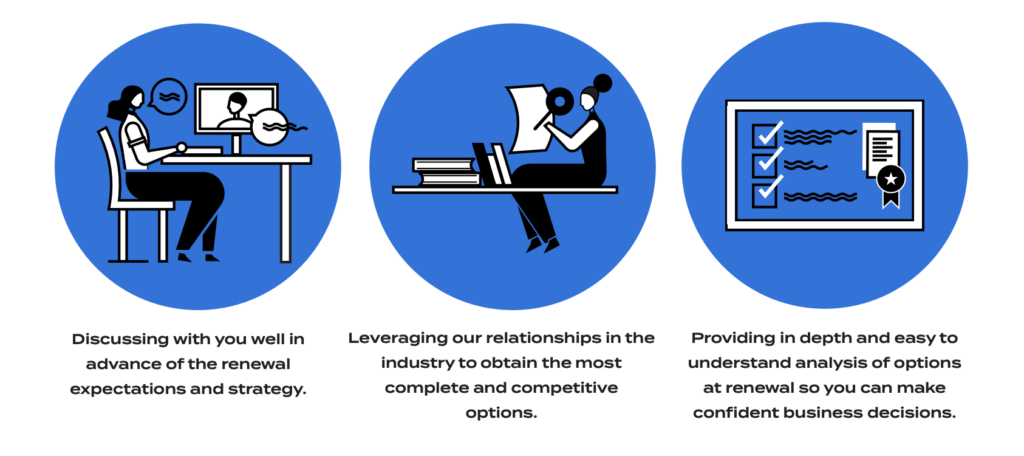

The BakerHopp Strategy

As your advisors in insurance and risk management, we are proactively prepared to work with you through any and all market adjustments. At BakerHopp Insurance Group, our core purpose is to contribute to the success of others— especially our clients. We understand that our role in your success is to provide transparent and competitive options with detailed information on changes in coverage and pricing so you can make informed business decisions. Our model of service below is the cornerstone of our capabilities:

Sources:

David Paul, “Property-Casualty Hard Market Turns 6,” Leader’s Edge, April 1, 2024, https://www.leadersedge.com/p-c/property-casualty-hard-market-turns-6

The Council of Insurance Agents & Brokers, “Q4 2023 P/C Market Survey,” https://www.ciab.com/resources/q4-2023-p-c-market-survey/

The Council of Insurance Agents & Brokers, “Premium Increases Flat to Down: CIAB Q1 2024 P/C Market Survey Shows,” https://www.ciab.com/resources/premium-increases-flat-to-down-ciab-q1-2024-p-c-market-survey-shows/

USI Insurance Services, “2024 P&C Mid-Year Market Outlook Addendum,” https://info.usi.com/rs/121-VCO-807/images/2024%20P%26C%20Mid-Yr%20Market%20Outlook%20Addendum.pdf